Dubai Real Estate Weekly Market Analysis 23-Feb-2026

- March 12, 2026

- 4

- News&Media

AHS Tower was the strongest performer this week delivering AED 761 million and 32 transactions.

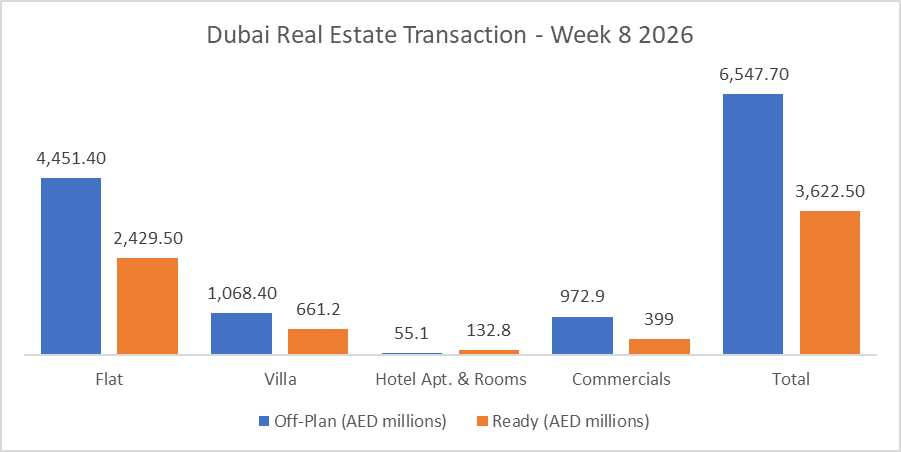

Total trading reached AED 10.2 bn in Week 8 across 4,184 transactions. Off-Plan dominated with AED 6.5 bn (64.4%), while Ready accounted for AED 3.6 bn (35.6%).

| Category | Off-Plan (AED millions) | Ready (AED millions) |

| Flat | 4,451.4 | 2,429.5 |

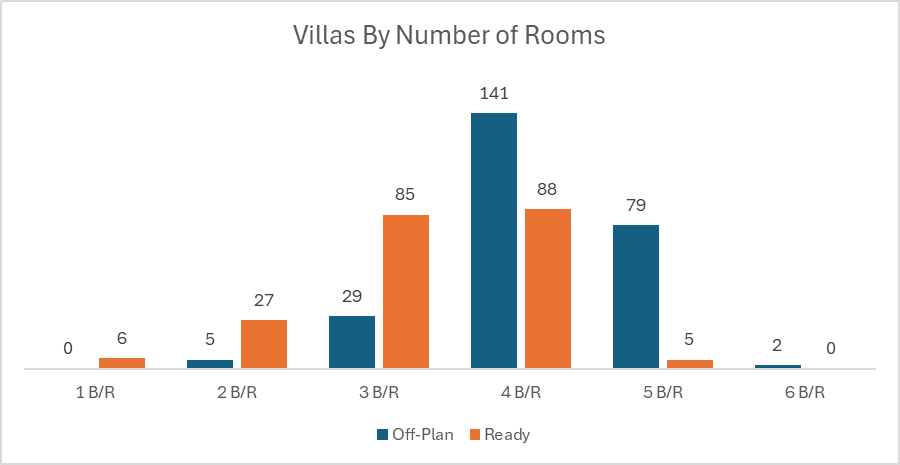

| Villa | 1,068.4 | 661.2 |

| Hotel Apt. & Rooms | 55.1 | 132.8 |

| Commercials | 972.9 | 399.0 |

| Total | 6,547.7 | 3,622.5 |

Off-Plan Market Performance

- Total Value: AED 6.5 bn

- Share of Weekly Total: 64.4%

| Sub-Category | Value (AED millions) | % of Off-Plan |

| Flat | 4,451.4 | 68.0% |

| Villa | 1,068.4 | 16.3% |

| Hotel Apt. & Rooms | 55.1 | 0.8% |

| Commercials | 972.9 | 14.9% |

Off-plan activity was flat-led, with commercials providing a meaningful secondary contribution.

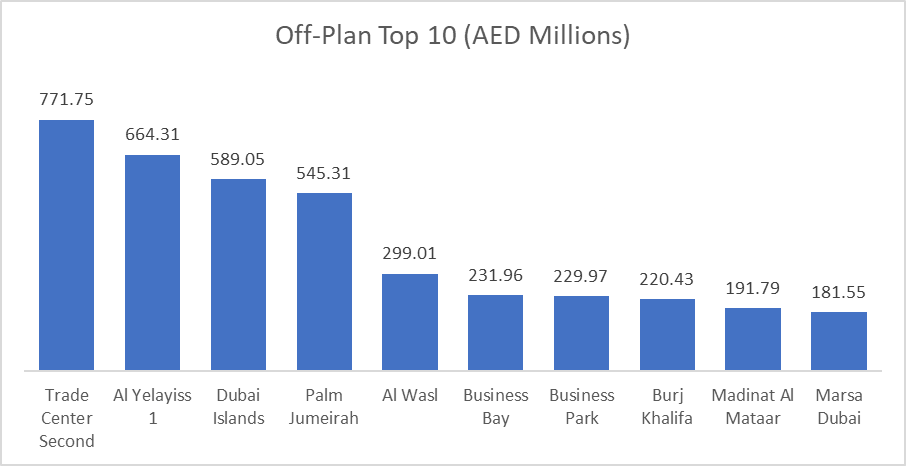

Top Performing Off-Plan Areas

Top 10 areas generated AED 3.9 bn (59.9% of Off-Plan value). It’s worth mentioning that the Trade Center Second transaction was concentrated in AHS Tower (offices).

| Area | Value (AED millions) | % of Off-Plan |

| Trade Center Second | 771.7 | 11.8% |

| Al Yelayiss 1 | 664.3 | 10.1% |

| Dubai Islands | 589.0 | 9.0% |

| Palm Jumeirah | 545.3 | 8.3% |

| Al Wasl | 299.0 | 4.6% |

Ready Market Performance

- Total Value: AED 3.6 bn

- Share of Weekly Total: 35.6%

| Sub-Category | Value (AED millions) | % of Ready |

| Flat | 2,429.5 | 67.1% |

| Villa | 661.2 | 18.3% |

| Hotel Apt. & Rooms | 132.8 | 3.7% |

| Commercials | 399.0 | 11.0% |

Ready market performance also skewed strongly toward flats, with villas as the clear runner-up.

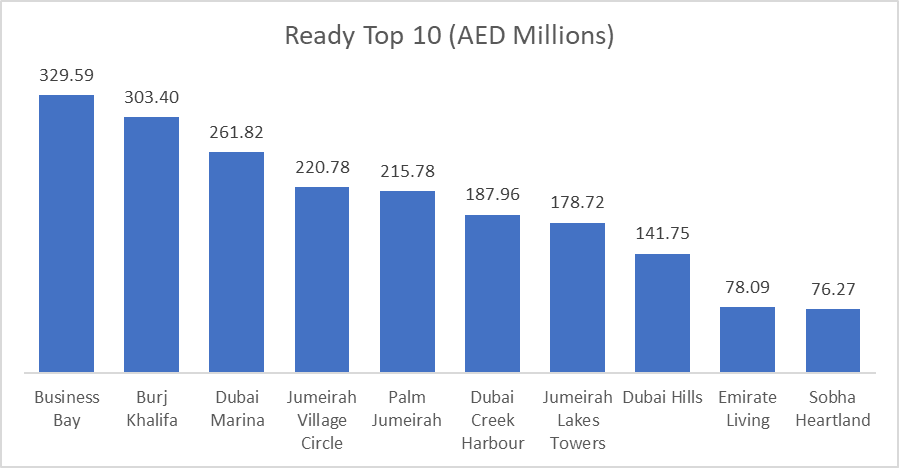

Top Performing Ready Areas

Top 10 areas generated AED 2.0 bn (55.0% of Ready value).

| Area | Value (AED millions) | % of Ready |

| Business Bay | 329.6 | 9.1% |

| Burj Khalifa | 303.4 | 8.4% |

| Dubai Marina | 261.8 | 7.2% |

| Jumeirah Village Circle | 220.8 | 6.1% |

| Palm Jumeirah | 215.8 | 6.0% |

On the Micro Level

Weekly Comparison

| Metric | Last Week | This Week | Change |

| Total Value (AED bn) | 14.1 | 10.2 | -3.9 bn (-27.9%) |

| Transactions | 5,481 | 4,184 | -1,297 (-23.7%) |

Market Insights & Outlook

Week 8 shows a broad cooling versus last week, with declines in both value (-27.9%) and transaction count (-23.7%), suggesting lower throughput, not just fewer large-ticket deals. Off-plan remained the market’s anchor at 64.4% of total value, and activity was highly concentrated: the top three off-plan areas (Trade Center Second, Al Yelayiss 1, Dubai Islands) delivered 30.9% of off-plan value, while the top three ready areas (Business Bay, Burj Khalifa, Dubai Marina) made up 24.7% of ready value. Palm Jumeirah featured in both segments’ top 10, reinforcing continued appetite for prime/coastal demand even during a softer weekly print.

Data Source: Dubai Land Department

Only freehold transactions are included