- April 23, 2026

- 5

- News&Media

Last week’s transactions value down 18.5% and number of transactions down 6.8%

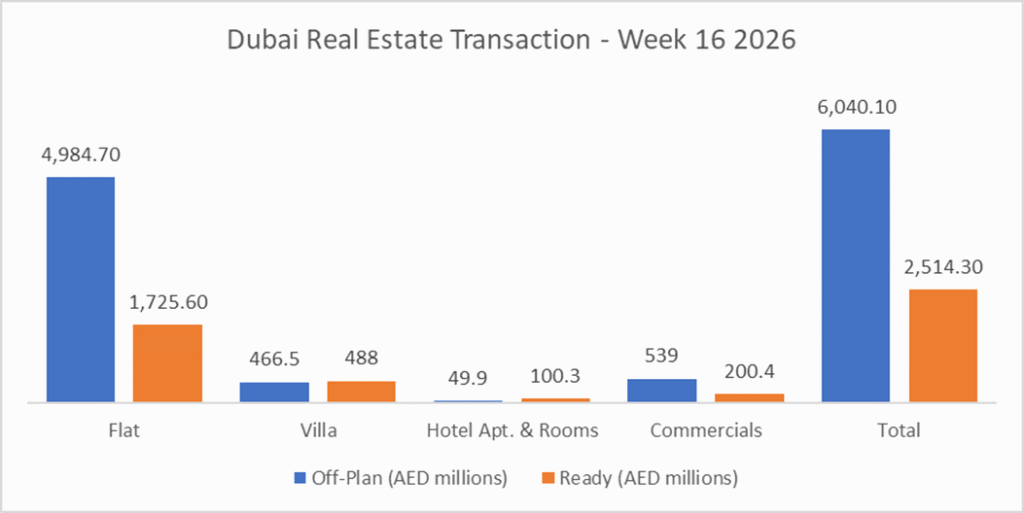

Total trading reached AED8.6 billion in Week 16 on an ex-land basis, down from AED10.5 billion in Week 15. Transaction activity also softened to 4,506 deals from 4,835, a decline of 329 transactions. Land sales added a further AED4.7 billion, taking the all-in weekly figure to roughly AED13.3 billion.

| Category | Off-Plan (AED millions) | Ready (AED millions) |

| Flat | 4,984.7 | 1,725.6 |

| Villa | 466.5 | 488.0 |

| Hotel Apt. & Rooms | 49.9 | 100.3 |

| Commercials | 539.0 | 200.4 |

| Total | 6,040.1 | 2,514.3 |

Off-Plan Market Performance

Total Value: AED6.0 billion

Share of Weekly Total: 70.6%

| Category | Value (AED millions) | % of Off-Plan |

| Flat | 4,984.7 | 82.5% |

| Villa | 466.5 | 7.7% |

| Hotel Apt. & Rooms | 49.9 | 0.8% |

| Commercials | 539.0 | 8.9% |

Off-plan remained the clear market driver, with flats alone contributing more than four-fifths of off-plan value, reinforcing how heavily primary-market demand is still skewed toward apartment-led launches and branded or waterfront stock. Villas made a much smaller but still meaningful contribution, while hotel apartments and rooms remained marginal.

From a transaction-type perspective, the off-plan market was overwhelmingly sales-led, with Sales accounting for AED5.94 billion, or 98.3% of off-plan value. Gifts contributed AED92.0 million (1.5%), while Mortgages were negligible at AED11.1 million (0.2%), underlining that the primary market continues to behave mainly as a direct sales market rather than a leveraged one.

Top Performing Off-Plan Areas

| Area | Value (AED millions) | Share of Off-Plan |

| Dubai Islands | 907.2 | 15.0% |

| Madinat Al Mataar | 554.8 | 9.2% |

| Jabal Ali First | 489.0 | 8.1% |

| Business Bay | 333.3 | 5.5% |

| Al Khairan First | 239.5 | 4.0% |

The top 10 areas in Off-Plan took 58.8% of the total Off-Plan transactions. The highest-value off-plan transactions were a flat in Palm Jumeirah for AED64.0 million and a villa in Madinat Al Mataar for AED21.0 million. These headline deals suggest that premium stock and large-format villa product continue to anchor the upper end of weekly primary-market activity.

Ready Market Performance

Total Value: AED2.5 billion

Share of Weekly Total: 29.4%

| Category | Value (AED millions) | % of Ready |

| Flat | 1,725.6 | 68.6% |

| Villa | 488.0 | 19.4% |

| Hotel Apt. & Rooms | 100.3 | 4.0% |

| Commercials | 200.4 | 8.0% |

The ready market remained secondary to off-plan, but it still posted a solid AED2.5 billion, with flats contributing 68.6% of the segment total. Villas accounted for 19.4%, while commercial assets and hotel apartments played smaller supporting roles. Compared with off-plan, the ready market showed a more balanced mix across sub-categories, particularly through a stronger villa and mortgage component.

Transaction-type analysis shows a very different structure from off-plan. In ready assets, Sales contributed AED1.16 billion (46.3%) and Mortgages were almost equally important at AED1.16 billion (46.0%), while Gifts added AED195.0 million (7.8%). That tells us the secondary market remains much more financing-driven and end-user or investor refinancing activity continues to underpin a large share of completed-property turnover.

Top Performing Ready Areas

| Area | Value (AED millions) | Share of Ready |

| Barsha Heights | 227.2 | 9.0% |

| Jumeirah Village Circle | 188.1 | 7.5% |

| Business Bay | 181.6 | 7.2% |

| Dubai Marina | 176.3 | 7.0% |

| Burj Khalifa | 141.2 | 5.6% |

The top 10 ready areas accounted for AED1.39 billion, or 55.2% of ready-market value. Barsha Heights alone represented around 9.0% of the ready segment, helped by the sale of 82 units, including shops, in the Tow Towers complex.

The highest-value ready transactions were a flat in Palm Jumeirah for AED27.5 million and a villa in Nad Al Shiba Gardens for AED17.68 million, again highlighting how Dubai’s completed prime residential stock continues to command outsized attention even in a softer week.

On the Micro Level

Weekly Comparison

| Metric | Last Week | This Week | Change |

| Total Value (AED billions) | 10.5 | 8.6 | -18.5% |

| Transactions | 4,835 | 4,506 | -6.8% |

Market Insights & Outlook

Week 16 marked a clear cooling from the previous week, with total ex-land trading falling by 18.5% and transaction volumes down 6.8%. Even so, the composition of demand remained familiar: off-plan dominated at 70.6% of weekly value, driven overwhelmingly by flat sales, while the ready market was supported by both direct sales and mortgage-backed transactions. The presence of AED4.7 billion in land deals also suggests that broader capital deployment into Dubai real estate remained substantial, even if the ex-land market lost some momentum. Overall, the week reads less like a structural slowdown and more like a step down in intensity, with activity still concentrated in core high-performing districts and premium-ticket assets.

Data Source: Dubai Land Department

Only freehold transactions are included