- April 16, 2026

- 2

- News&Media

Weekly trading value was stable with slightly higher number of transactions

Total trading reached AED 10.49 billion across 4,835 transactions in Week 15, compared with AED 10.59 billion and 4,636 transactions in the prior week. That means weekly value edged down by 0.9%, while transaction count increased by 4.3%, pointing to a busier market but with a lower average ticket size.

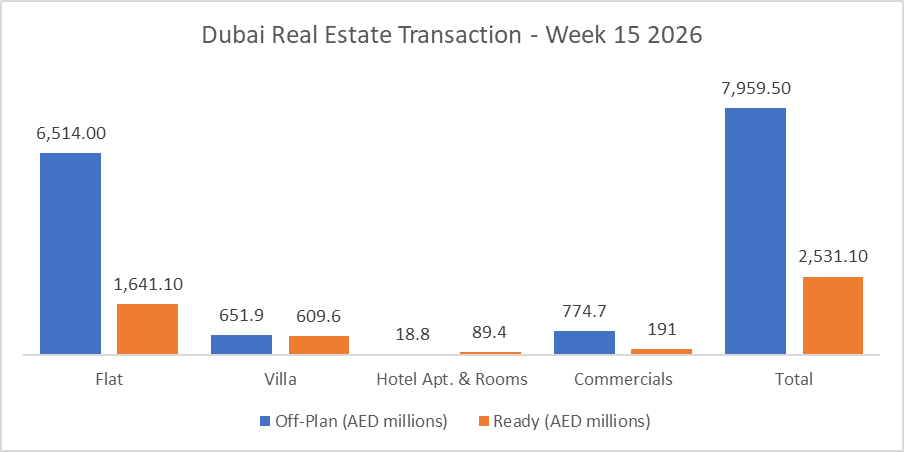

| Category | Off-Plan (AED millions) | Ready (AED millions) |

| Flat | 6,514.0 | 1,641.1 |

| Villa | 651.9 | 609.6 |

| Hotel Apt. & Rooms | 18.8 | 89.4 |

| Commercials | 774.7 | 191.0 |

| Total | 7,959.5 | 2,531.1 |

Off-Plan Market Performance

Total Value: AED 7.96 billion

Share of Weekly Total: 75.9%

Off-plan remained the clear driver of the market in Week 15, contributing more than three-quarters of all traded value. The segment was heavily led by flats, while commercial assets also made a meaningful contribution, helping keep the off-plan mix broad rather than dependent on one product type alone.

| Sub-Category | Value (AED millions) | % of Off-Plan |

| Flat | 6,514.0 | 81.8% |

| Villa | 651.9 | 8.2% |

| Hotel Apt. & Rooms | 18.8 | 0.2% |

| Commercials | 774.7 | 9.7% |

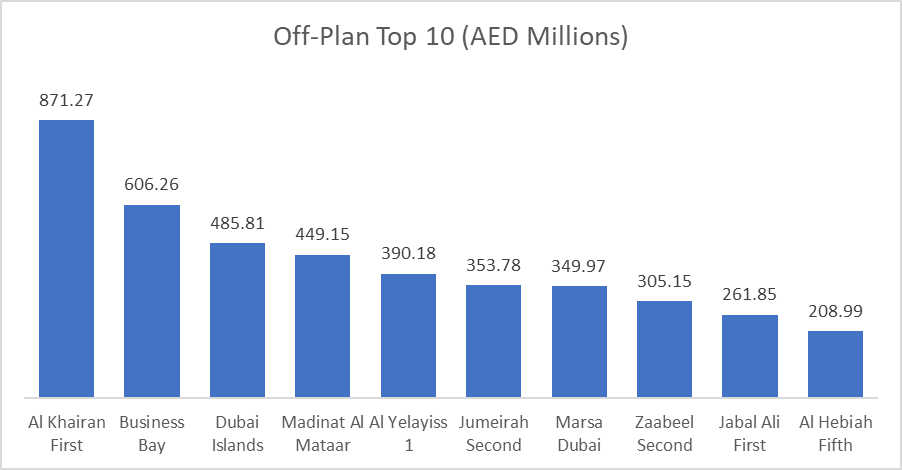

Top Performing Off-Plan Areas

| Area | Value (AED millions) |

| Al Khairan First | 871.3 |

| Business Bay | 606.3 |

| Dubai Islands | 485.8 |

| Madinat Al Mataar | 449.2 |

| Al Yelayiss 1 | 390.2 |

The top 10 off-plan areas generated AED 4.28 billion, equal to roughly 53.8% of all off-plan value. Al Khairan First led the market with AED 871.3 million, or about 10.9% of total off-plan trading, followed by Business Bay and Dubai Islands.

Ready Market Performance

Total Value: AED 2.53 billion

Share of Weekly Total: 24.1%

Ready sales accounted for just under a quarter of weekly value. While much smaller than off-plan, the ready segment showed a more balanced internal mix, with villas and hotel apartments taking a more visible share than they did in off-plan.

| Sub-Category | Value (AED millions) | % of Ready |

| Flat | 1,641.1 | 64.8% |

| Villa | 609.6 | 24.1% |

| Hotel Apt. & Rooms | 89.4 | 3.5% |

| Commercials | 191.0 | 7.5% |

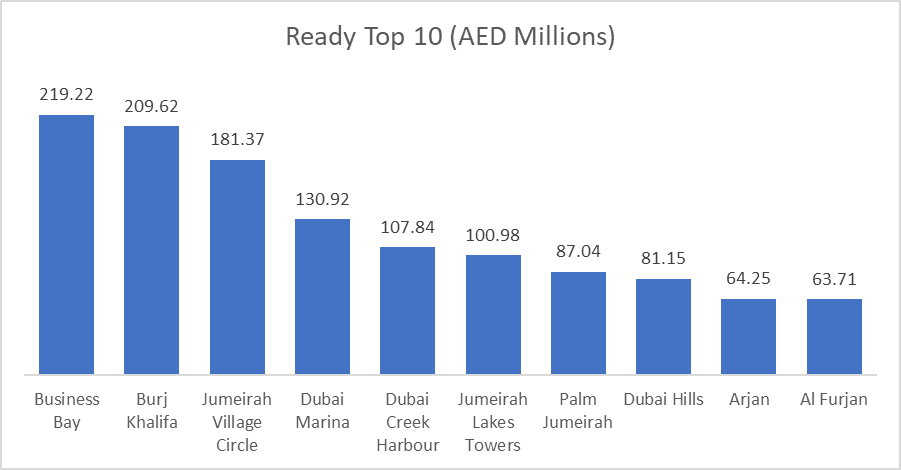

Top Performing Ready Areas

| Area | Value (AED millions) |

| Business Bay | 219.2 |

| Burj Khalifa | 209.6 |

| Jumeirah Village Circle | 181.4 |

| Dubai Marina | 130.9 |

| Dubai Creek Harbour | 107.8 |

The top 10 ready areas generated AED 1.25 billion, representing around 49.2% of all ready-market value. Business Bay ranked first at AED 219.2 million, narrowly ahead of Burj Khalifa at AED 209.6 million, showing continued concentration in established urban, high-liquidity locations.

On the Micro Level

Transaction-type analysis shows that sales remained overwhelmingly dominant, accounting for AED 9.18 billion, or roughly 87.5% of the ex-land weekly total. Within off-plan, sales made up 98.6% of segment value, confirming that new-launch and primary market demand remained the key force behind weekly activity.

In the ready market, the structure was more varied. Sales contributed 52.4% of ready value, while mortgages accounted for a significant 39.7%, equal to just over AED 1.00 billion. This is an important signal: unlike off-plan, ready activity was supported not only by outright purchases but also by financing-led transactions. Gifts were also notable, contributing AED 200.9 million in ready and AED 83.9 million in off-plan.

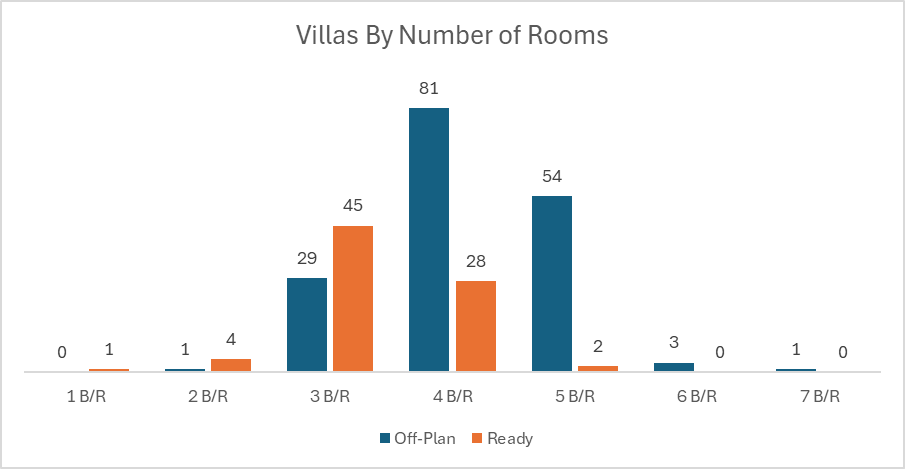

At the individual deal level, the highest-value transactions underline where premium demand sat this week. In off-plan, the top flat deal was in Jumeirah Second at AED 171.0 million, while the top villa deal came from Madinat Al Mataar at AED 22.9 million. In ready, the highest flat transaction was recorded in Burj Khalifa at AED 30.0 million, and the top villa transaction was in Island 2 at AED 21.5 million.

Weekly Comparison

| Metric | Last Week | This Week | Change |

| Total Value (AED billions) | 10.59 | 10.49 | -0.9% |

| Transactions | 4,636 | 4,835 | +199 |

| Average Value per Transaction (AED millions) | 2.28 | 2.17 | -5.0% |

Market Insights & Outlook

Week 15 presented a market that was broader in participation but slightly lighter in value. The decline in headline volume was marginal, yet the rise in transaction count suggests activity stayed healthy and that the slowdown came more from ticket size than from weakening demand.

The key takeaway remains the same: Dubai’s market is still being carried by off-plan, especially flats, with the top off-plan areas capturing deep investor interest across both established and emerging development corridors. At the same time, the ready market continues to show resilience through a combination of end-user sales, financing activity, and high-value trades in mature trophy districts such as Business Bay and Burj Khalifa.

Overall, Week 15 was not a weak week. It was a slightly softer value week inside a still-active market, with off-plan continuing to dominate the headline story and ready transactions adding depth through mortgage-backed and premium-location activity.

Data Source: Dubai Land Department

Only freehold transactions are included