- April 17, 2026

- 2

- News&Media

Land transactions in Nov. 2024 was 38.7% of the total transactions. The market saw a decrease of approximately AED 20 billion from Oct 2024 to Nov. 2024, and up AED 1.2 billion from Nov. 2023.

In November 2024, the total value of transactions in the real estate market reached approximately AED 54.0 billion. This represents a significant decrease compared to last month’s figure of AED 74.1 billion and is slightly lower than the November 2023 total of AED 55.2 billion, suggesting a period of consolidation or cautious investor sentiment.

Breakdown by Segment

- Off-Plan Properties:

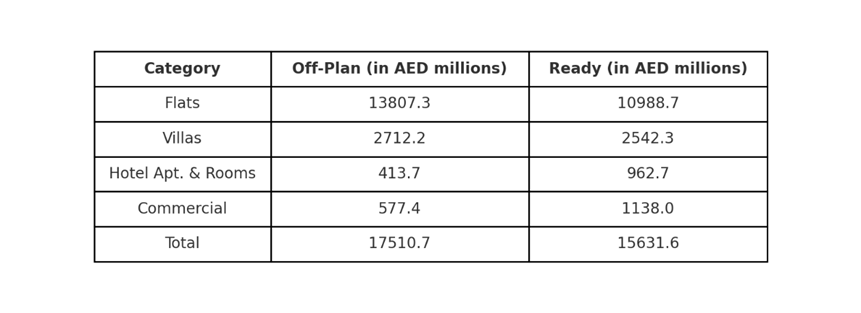

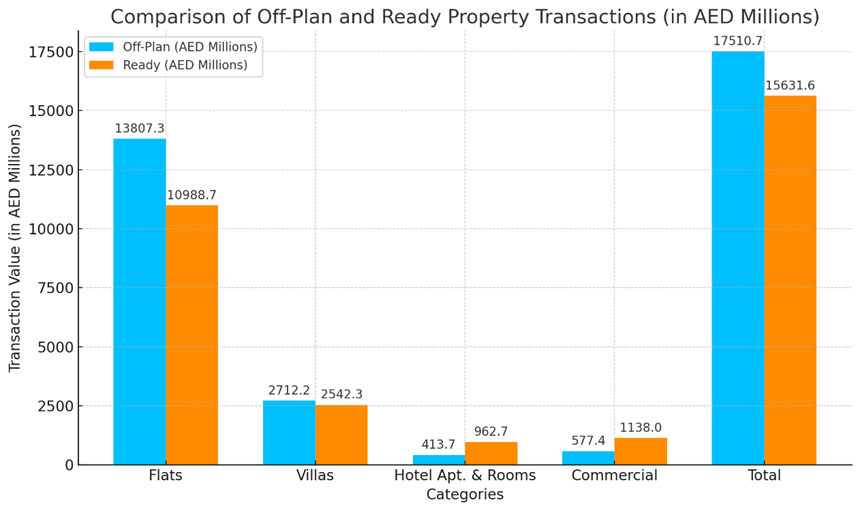

Total off-plan transactions amounted to AED 17.5 billion, with flats taking the lion’s share at AED 13.8 billion. Villas contributed AED 2.7 billion, followed by hotel apartments and rooms at AED 413.7 million, and shops and offices at AED 577.4 million. The robust off-plan performance continues to highlight investor confidence in upcoming projects, although the segment’s share this month is lower than some previous peak periods. - Ready Properties:

Ready properties contributed AED 15.6 billion to the total. Flats once again dominated, with AED 11.0 billion in value, while villas accounted for AED 2.5 billion. Hotel apartments and rooms registered AED 962.7 million, and shops and offices reached AED 1.14 billion. The ready market’s performance indicates steady end-user and investor interest in immediately deliverable units. - Land Transactions:

Land sales totaled a strong AED 20.9 billion. This segment’s stability points to ongoing confidence in long-term investment and development potential, as investors and developers position themselves for future market cycles.

Comparison to Prior Periods

- Versus October 2024 (AED 74.1 billion):

November’s AED 54.0 billion total marks a noticeable pullback from the high transaction volumes seen just a month prior. This could be attributed to a variety of factors including seasonal slowdowns, the conclusion of high-profile project launches in the previous months, or a measured pause as investors re-evaluate market conditions. - Versus November 2023 (AED 55.2 billion):

Year-over-year, the market is down slightly by approximately AED 1.2 billion. While the difference is modest, it may signal a more mature phase of market growth, with investors adopting a more selective and value-focused approach rather than engaging in broad-based purchasing.

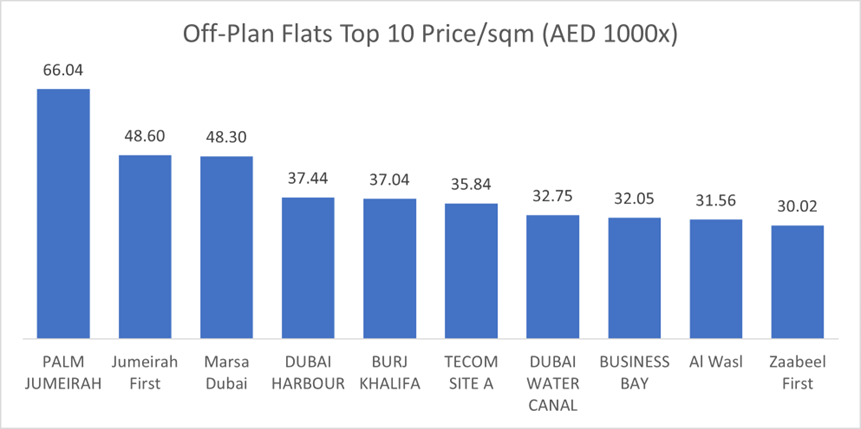

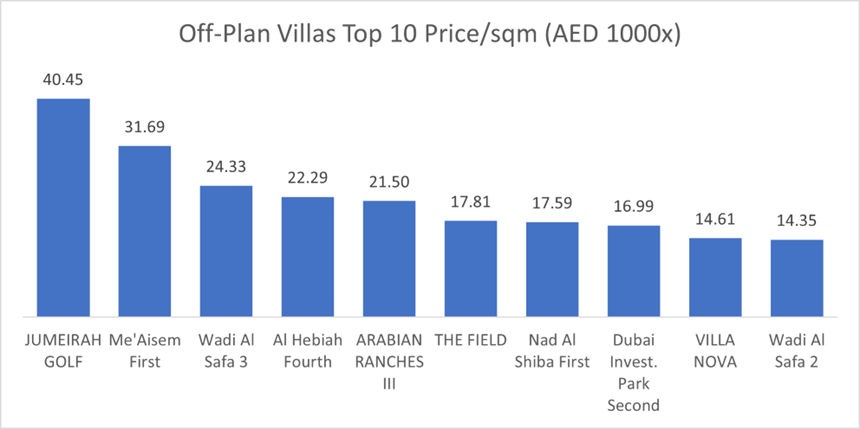

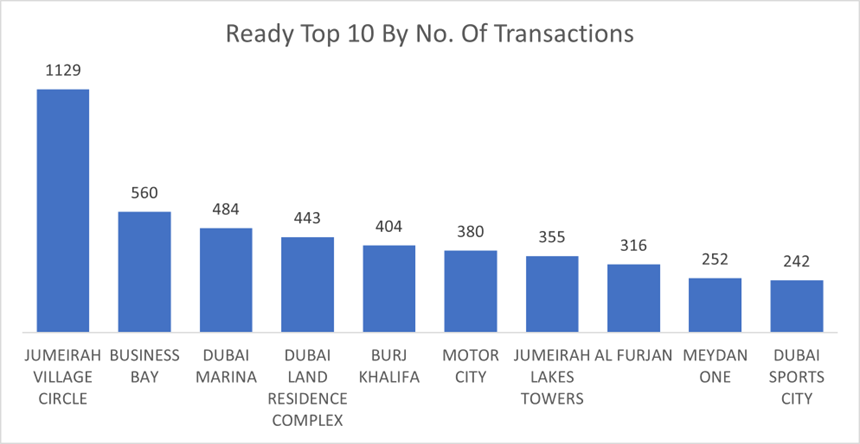

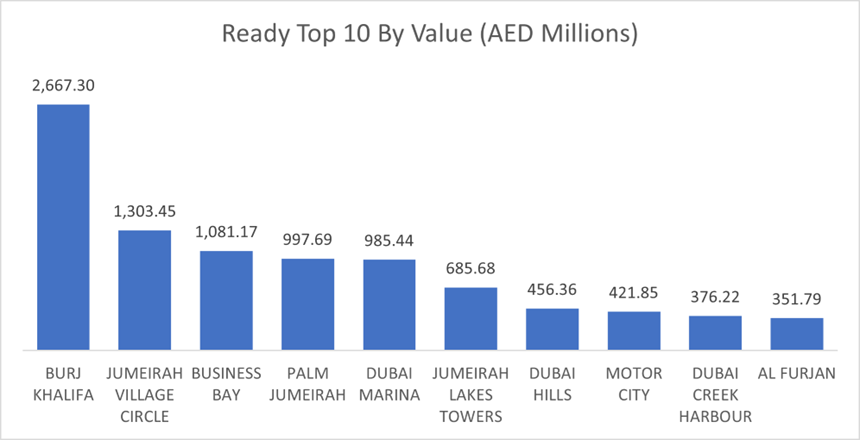

Top Performing Areas

Following the overall market overview, certain communities continued to capture investor interest and transaction volumes during November 2024. A closer look at the top areas by number of transactions and total value reveals ongoing demand in both established neighborhoods and emerging hotspots.

Key Insights

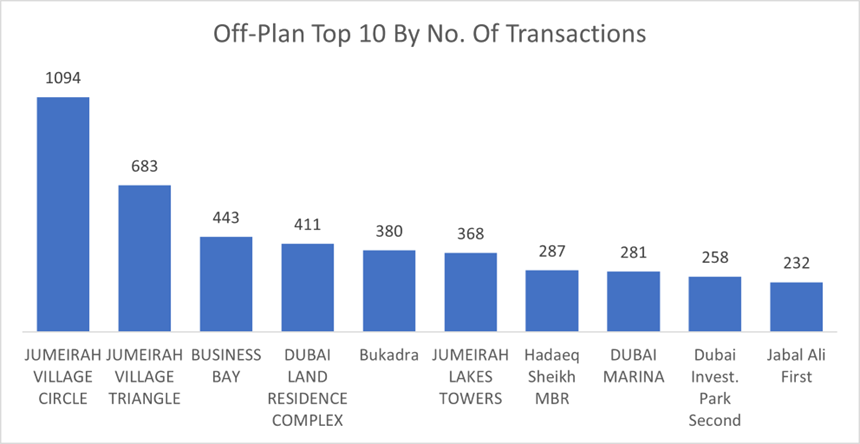

- Jumeirah Village Circle (JVC):

- Dominates both off-plan and ready segments by number of transactions

- Attractive to a wide range of buyers due to its affordability and variety of unit types

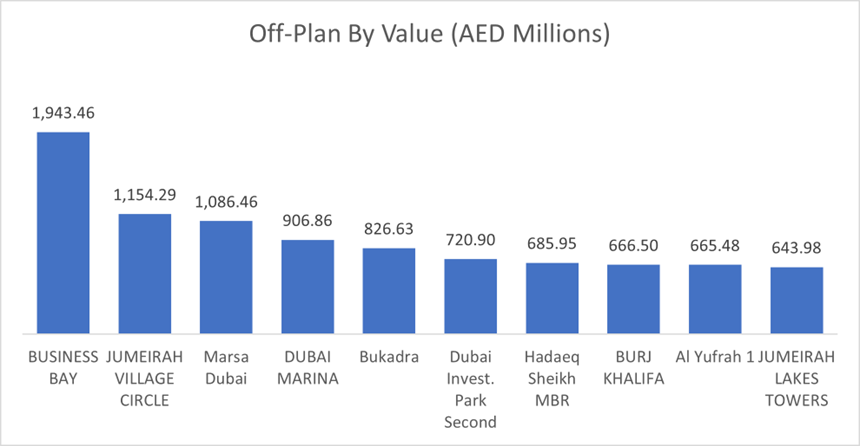

- Business Bay & Burj Khalifa Area:

- High transaction values in off-plan (Business Bay) and ready (Burj Khalifa) markets

- Reflect demand for prime, centrally located, and iconic properties

- Established vs. Emerging Areas:

- Mature locales like Dubai Marina, Palm Jumeirah, and Jumeirah Lakes Towers continue to command strong values

- Up-and-coming neighborhoods such as Al Yufrah 1 and Bukadra are also gaining traction, indicating a broad-based market appeal

Outlook

The November 2024 numbers suggest that the market is undergoing a period of adjustment after experiencing robust activity in recent months. Going forward, the balance between off-plan enthusiasm, steady absorption of ready units, and enduring interest in land transactions will shape the trajectory. Market participants will likely monitor macroeconomic indicators, upcoming project announcements, and policy frameworks closely, as these factors influence both short-term sentiment and long-term market stability. Overall, November 2024 shows a more measured pace compared to previous periods, with a healthy distribution of investments across a range of established and evolving communities.