- April 22, 2026

- 4

- News&Media

The total real estate transactions in Dubai for Week 48 were AED 11.30 billion and 5,457 transactions. Off plan contributed 58.7% or 6.64 billion, while Ready properties contributed 41.3% or 4.66 billion.

Total trading in Week 48 reached AED 11.30 billion this week across 5,457 transactions, a mild 1.6% dip in value from last week’s AED 11.48 billion, while transaction volumes were up 3.3%. Off plan continued to lead the market, accounting for 58.7% of total value, with ready properties contributing the remaining 41.3%.

| Category | Off-Plan (AED millions) | Ready (AED millions) |

| Flat | 5,806.3 | 3,021.0 |

| Villa | 463.5 | 983.1 |

| Hotel Apt. & Rooms | 17.1 | 157.8 |

| Commercials | 349.8 | 499.4 |

| Total | 6,636.7 | 4,661.3 |

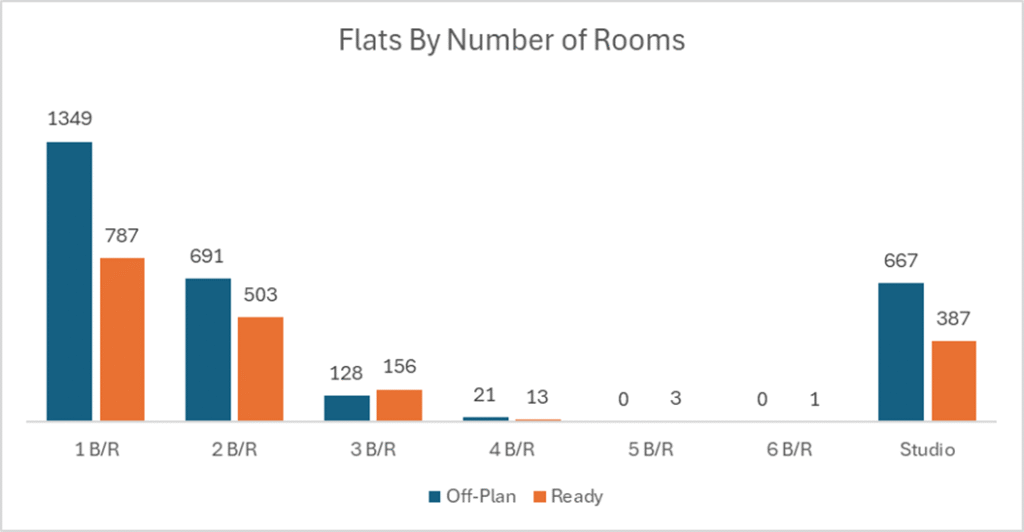

Flats dominate the week’s activity with more than three-quarters of all value traded, while villas remain the clear second pillar of demand.

Off-Plan Market Performance

Total Value: AED 6.64 billion

Share of Weekly Total: 58.7%

Off plan retained its leadership this week, driven overwhelmingly by apartment launches, with villas playing a secondary but still meaningful role.

Off-Plan by Property Type

| Category | Value (AED millions) | % of Off-Plan |

| Flat | 5,806.3 | 87.5% |

| Villa | 463.5 | 7.0% |

| Hotel Apt. & Rooms | 17.1 | 0.3% |

| Commercials | 349.8 | 5.3% |

| Total Off-Plan | 6,636.7 | 100.0% |

Off-plan activity is highly concentrated in flats, which contributed nearly nine dirhams out of every ten in the off-plan segment. Villas added another 7.0%, while commercial and hospitality stock remain niche but strategically important components.

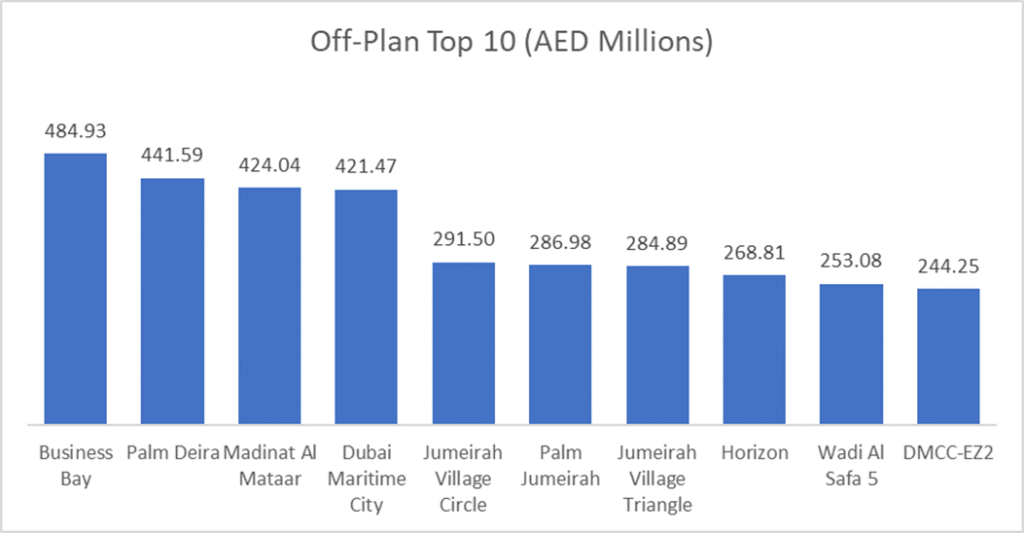

Top Performing Off-Plan Areas

| Area | Value (AED millions) | % of Off-Plan Value |

| Business Bay | 484.9 | 7.3% |

| Palm Deira | 441.6 | 6.7% |

| Madinat Al Mataar | 424.0 | 6.4% |

| Dubai Maritime City | 421.5 | 6.4% |

| Jumeirah Village Circle | 291.5 | 4.4% |

Off-plan demand is heavily focused on mixed-use and emerging waterfront districts: Business Bay, Palm Deira, Madinat Al Mataar and Dubai Maritime City alone represent over a quarter of off-plan value. JVC, JVT and Horizon show that mid-market community living continues to attract a substantial slice of new-buyers and investors.

Ready Market Performance

Total Value: AED 4.66 billion

Share of Weekly Total: 41.3%

The ready segment provided a solid counterweight to off-plan, with meaningful depth across both apartments and villas and a visible bias toward prime and established communities.

Ready by Property Type

| Category | Value (AED millions) | % of Ready |

| Flat | 3,021.0 | 64.8% |

| Villa | 983.1 | 21.1% |

| Hotel Apt. & Rooms | 157.8 | 3.4% |

| Commercials | 499.4 | 10.7% |

| Total Ready | 4,661.3 | 100.0% |

Within ready, flats account for nearly two-thirds of value, but villas contribute over one-fifth, confirming continued appetite for end-user and lifestyle-driven purchases. Ready commercial assets captured 10.7% of ready value, highlighting ongoing demand for income-generating stock.

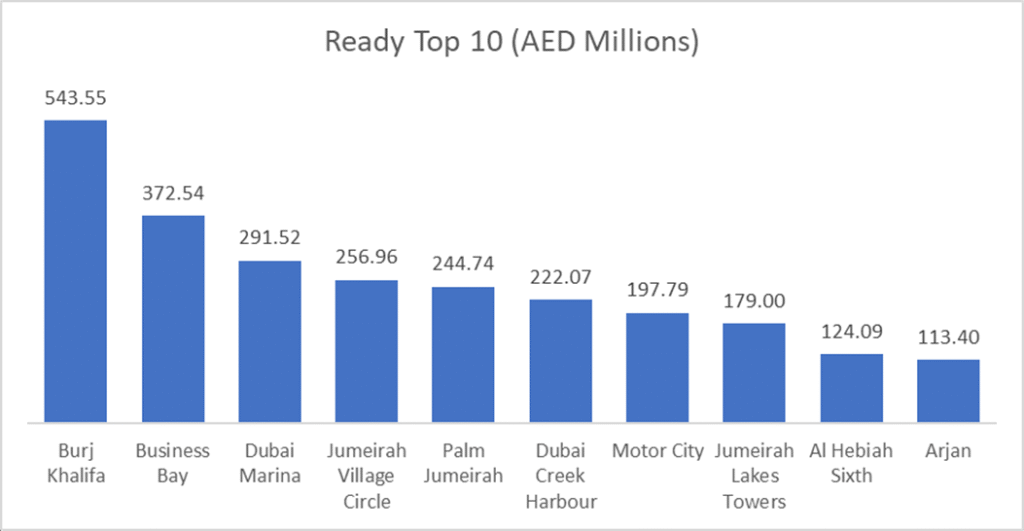

Top Performing Ready Areas

| Area | Value (AED millions) | % of Ready Value |

| Burj Khalifa | 543.6 | 11.7% |

| Business Bay | 372.5 | 8.0% |

| Dubai Marina | 291.5 | 6.3% |

| Jumeirah Village Circle | 257.0 | 5.5% |

| Palm Jumeirah | 244.7 | 5.3% |

Ready trading was led by Burj Khalifa and Business Bay, underscoring depth in the Downtown–Business Bay corridor, while Dubai Marina, Palm Jumeirah and Dubai Creek Harbour confirm that waterfront and high-density lifestyle hubs remain the core of the secondary market.

On the Micro Level

Weekly Comparison

| Metric | Last Week | This Week | Change |

| Total Traded Value (AED billions) | 11.48 | 11.30 | -1.6% |

| Number of Transactions | 5,457 | 5,284 | 3.3% |

Market Insights & Outlook

This week’s data paints a picture of a two-speed market:

- Off-plan remains the primary growth engine, contributing 58.7% of all traded value and being driven overwhelmingly by apartment-led launches. The concentration in Business Bay, Palm Deira, maritime and airport-adjacent districts suggest investors are leaning into infrastructure-led and regeneration stories.

- Ready stock continues to appeal to both end-users and yield-focused investors, with prime vertical living (Burj Khalifa, Marina, JLT) and branded/waterfront communities (Palm Jumeirah, Creek Harbour) absorbing substantial capital.

With total value only marginally lower week-on-week and deal volumes stable, the market appears to be in a phase of healthy digestion rather than a slowdown. If new off plan launches remain disciplined and ready supply continues to recycle in core districts, the coming weeks should see similarly high but more selective trading, with micro-location and project quality acting as the main differentiators for performance.

Data Source: Dubai Land Department