- April 21, 2026

- 2

- News&Media

Indian-owned businesses lead new non-UAE company registrations. Followed by Pakistan and Egypt, Bangladesh was the fastest growing.

Samana Developers sells out Samana Hills South 2 in Dubai South

Samana Developers sold out Samana Hills South 2 in Dubai South, 140 units across two six-storey towers, within 90 minutes. Prices start at AED 599,000, with handover due October 2028. The developer cites a surging off-plan market; it ranked fifth in H1 2025, hitting AED 1.1bn June sales.

Indian-owned businesses lead new non-UAE company registrations in Dubai with 9,038 members in H1 2025

Dubai Chamber data shows Indian-owned firms led new registrations in H1 2025 with 9,038 members (+14.9%). Pakistan and Egypt followed; Bangladesh saw fastest growth (+37.5%). Top sectors: wholesale/retail and real estate (35% each). UAE counts 264,687 Indian companies; manufacturing is 13.5% of non-oil GDP.

Dubai property market enters new era with BT-AI Broker Terminal

BT-AI: Broker Terminal launches in Dubai to restore trust in real estate, offering WhatsApp-based access to AI-powered sales data, appraisals, fees, developer profiles, ROI tools, and vetted brokers. Founded by Nadeem Tariq and team, it serves buyers, sellers, developers, and investors with ethics-led transparency.

Azizi Developments celebrates handover of Azizi Azure in Riviera, MBR City

Azizi Developments began handing over Azizi Azure, part of Azizi Riviera (phase four) in MBR City, following buildings 61, 63, 65 and 67. This brings Riviera’s delivered buildings to 54. The French-Mediterranean community will comprise 75 buildings (16,000 homes) with retail boulevard, lagoon walk and Les Jardins.

UAE property market sizzles as investors turn to Dubai

Despite global uncertainty, UAE real estate booms, led by Dubai. Tax-free income, high yields and pro-business policies attract expats and HNWIs. Market centers on off-plan projects and luxury; commissions are strong. Regulation is robust, Golden Visas help; RAK’s 2027 Wynn resort signals wider growth.

Sold out: Wasl’s South Garden D & E sparks unprecedented buyer demand

Wasl Group launched South Garden Buildings D & E at Wasl Gate, adding studios to 3-bed apartments with premium amenities and Festival Plaza access. Strategically on Sheikh Zayed Road near Energy Metro. Some units reserved for Dubai FTHB (under AED 5m), emphasizing value and strong connectivity.

Dubai’s RTA launches 5 new public bus routes, upgrades 9 others to meet growing demand

Dubai RTA will launch five new bus routes and enhance nine from August 29 to improve connectivity. New services: 31, 62A/62B, F26A (Al Quoz) and express X91; peak intervals 20–30 minutes. Several routes shortened or made two-directional to streamline travel.

Emirates REIT Ends H1 With a Strong Balance Sheet at 20% LTV, and 24% Increase in the Properties’ Income

Emirates REIT’s H1 2025: record 95% occupancy, rents +14%, total property income $39m; net property income $34m (+24%). LTV cut to 20% (from 40%); net finance costs down 57% to $12m after asset sales/refi. $7m dividend paid; $177m revaluation lifted assets to $1.2bn.

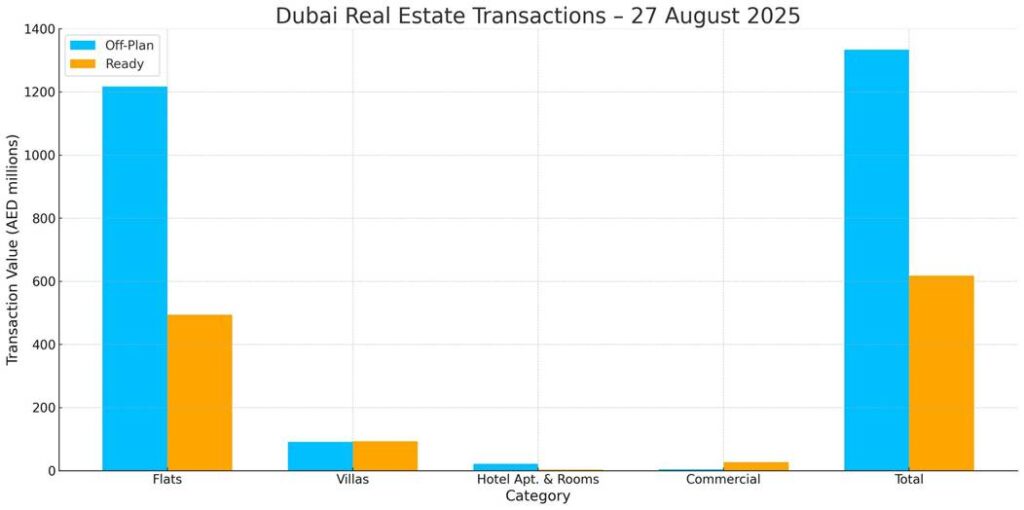

Dubai Real Estate Transactions as Reported on the 27th of August 2025

Dubai recorded AED 1.95bn in real estate transactions. Off-plan accounted for 68.3% (AED 1.334bn), outpacing Ready at 31.7% (AED 618.2m), about 2.16× more by value. Activity was led by flats in both segments.

| Category | Off-Plan (AED millions) | Ready (AED millions) |

| Flats | 1,217.4 | 494.1 |

| Villas | 91.5 | 93.2 |

| Hotel Apt. & Rooms | 21.4 | 3.7 |

| Commercial | 3.9 | 27.1 |

| Total | 1,334.1 | 618.2 |

Off-Plan Market Performance

Total: AED 1,334.1m (68.3% of day’s total)

- Flats: AED 1,217.4m (91.3% of off-plan)

- Villas: AED 91.5m (6.9%)

- Hotel Apts & Rooms: AED 21.4m (1.6%)

- Commercial: AED 3.9m (0.3%)

Off-plan was overwhelmingly flat-driven, with villas a distant second; hospitality and commercial were marginal.

Ready Market Performance

Total: AED 618.2m (31.7% of day’s total)

- Flats: AED 494.1m (79.9% of ready)

- Villas: AED 93.2m (15.1%)

- Hotel Apts & Rooms: AED 3.7m (0.6%)

- Commercial: AED 27.1m (4.4%)

Ready activity was broad-based but still dominated by flats; commercial contributed a modest share.

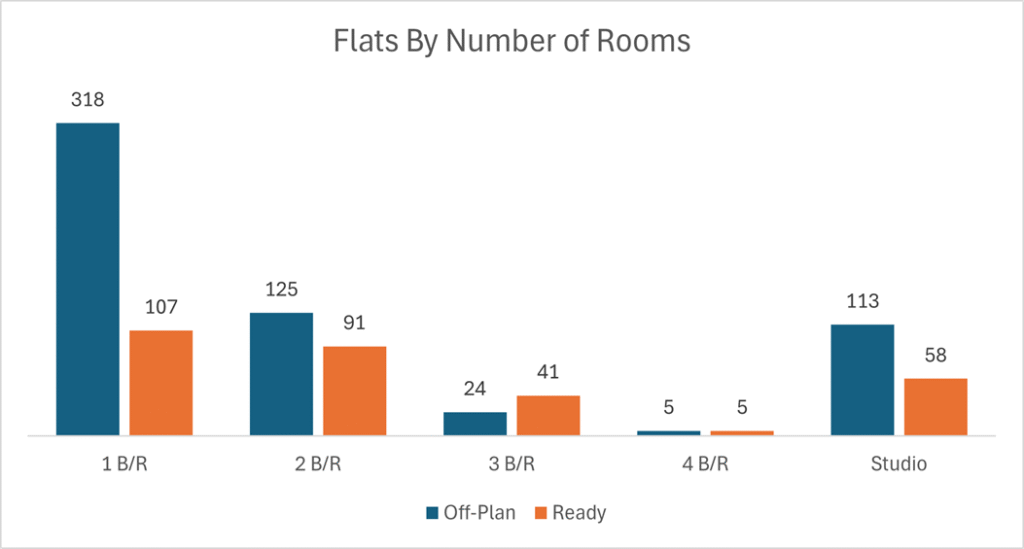

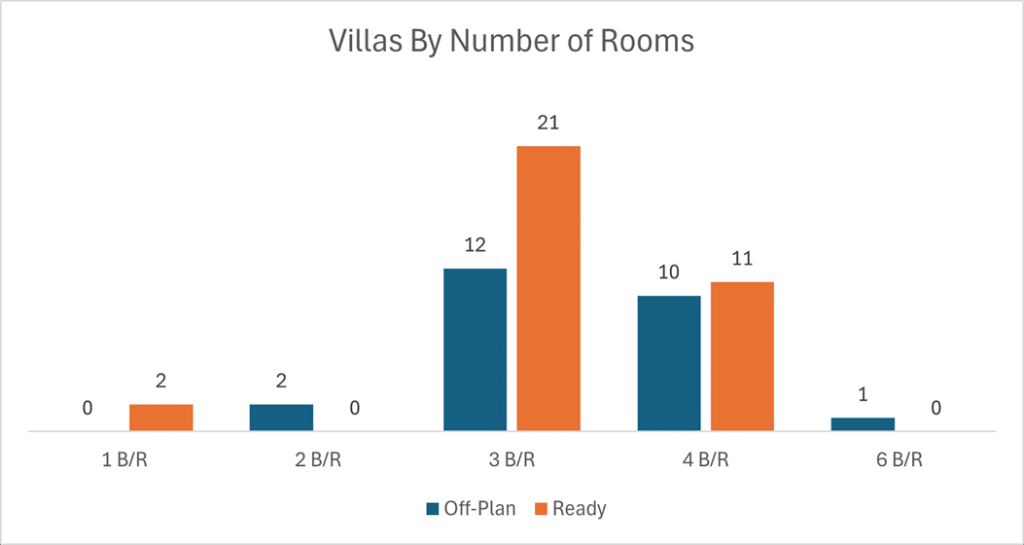

On The Micro Level

Market Insights & Outlook

- Flat dominance across both segments underscores end-user and investor preference for apartments, with off-plan launches capturing the bulk of value.

- Villas remain supportive, particularly in the ready market, but trail apartments by a wide margin.

- Thin hospitality/commercial prints suggest a residential-led day; watch for upcoming project releases to sustain off-plan momentum.

- Overall mix points to continued confidence in off-plan while ready transactions provide liquidity for immediate occupancy buyers.